Outperformance amidst market uncertainty

Strong operating performance resulted in generally positive returns for the first quarter of 2025 across real estate, credit, and venture capital.

Note: The original investor letter was published April 2, 2025 before the announcement of the U.S. new tariff policies, however we feel the events of the past week only further support the majority of the forecasts shared below.

- Strong performance supports our 2025 outlook: Fundrise portfolios outperformed the stock market in Q1 2025, a trend we expect to continue going forward.

- Real estate fundamentals remain solid: The right assets (residential and industrial) in the right markets (Sunbelt) continue to drive positive results.

- Valuations favor private markets: Despite recent losses, stocks are still at historically high valuations, while real estate assets, which have already reset, remain relatively affordable.

- Policy shifts create opportunity: We expect new administration policies, such as tariffs, are likely to benefit real estate values over the near term.

Q1 performance: Stability when it matters

We began the year making the case that we expected returns for real estate and other private assets, particularly the Fundrise portfolio, to outperform the stock market in 2025.

Through the first quarter this has proven true with the majority of clients across all three of the platform's primary asset strategies; real estate, private credit, and venture capital, experiencing positive returns while the stock market had its first negative quarter since late 2022.

This can largely be attributed to two things:

- Strong fundamentals at the property level: We continue to believe that the Fundrise portfolio consists of the right assets (residential and industrial) in the right markets (the Sunbelt).

- Timing advantage in the rate cycle: Real estate has already experienced much of the negative impacts of higher interest rates, and is now positioned to benefit from falling rates due to a slowing economy. Stocks, on the other hand, arguably had not seen the same negative impact and even after the recent steep declines remain precariously overvalued in the face of ever-increasing economic headwinds.

As we look ahead, we continue to see a compelling case for both real estate specifically and private markets more broadly to outperform. On a historical basis both still look relatively cheap when compared to public equities.

Additionally, we believe the near-term impacts of many of the new administration's policies (which we expect to result in slower growth, lower rates, and higher construction costs) will in turn lead to higher values for most real estate assets, especially properties such as those within the Fundrise portfolio which are already benefitting from larger secular tailwinds.

In other words, the policies and economic dynamics that were depressing real estate and boosting stocks have now almost completely reversed. Going forward we expect the mirror-opposite policies are likely to have the mirror-opposite impact, boosting real estate and depressing stocks. (The initial impact of the new tariff policies appears to be supporting this belief.)

The old adage of buy low and sell high is easy to say and hard to do. But during certain periods, as we feel is true today, it becomes increasingly important — especially for those investors looking to protect the gains they’ve made over the past several years from future volatility.

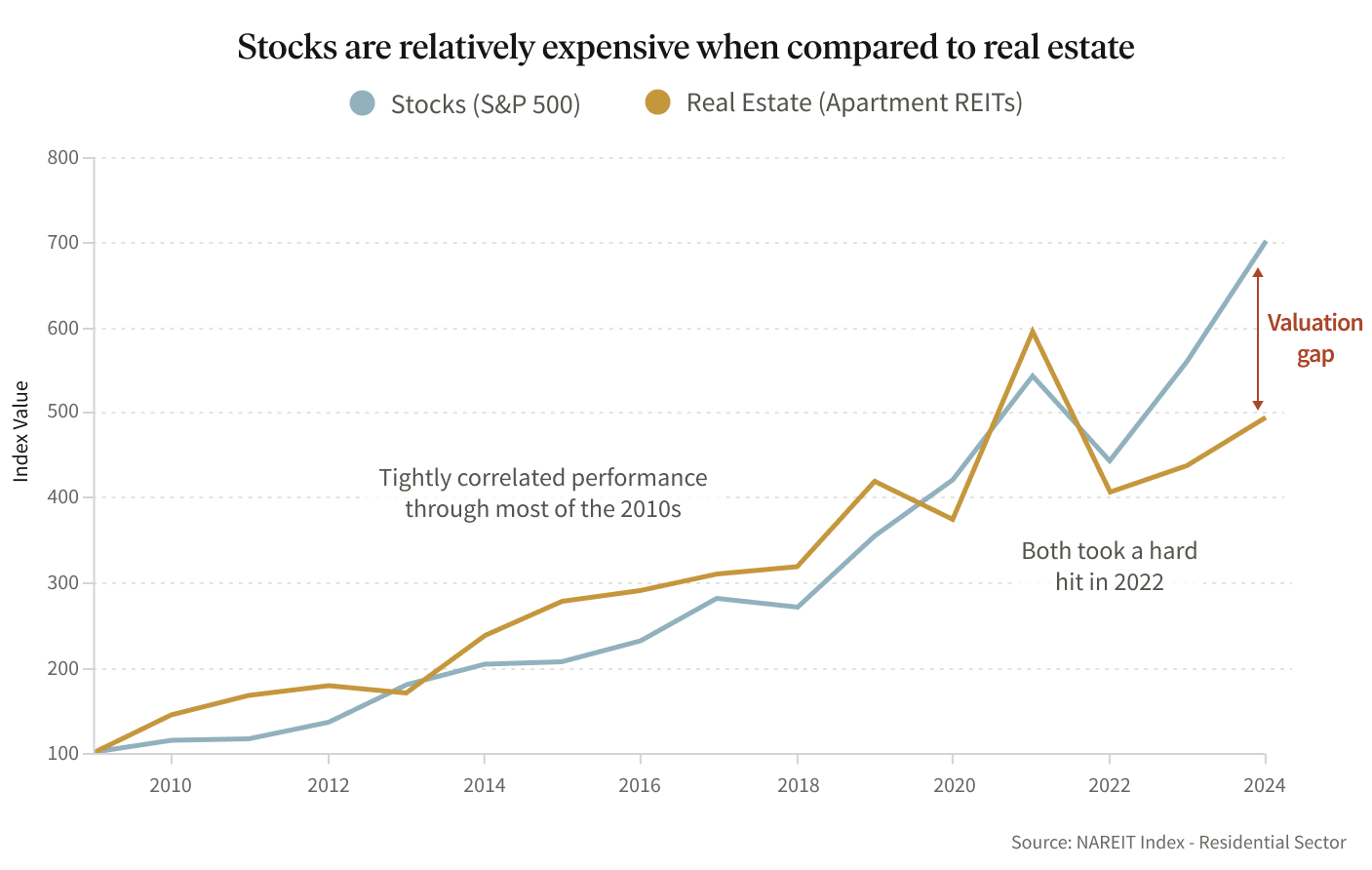

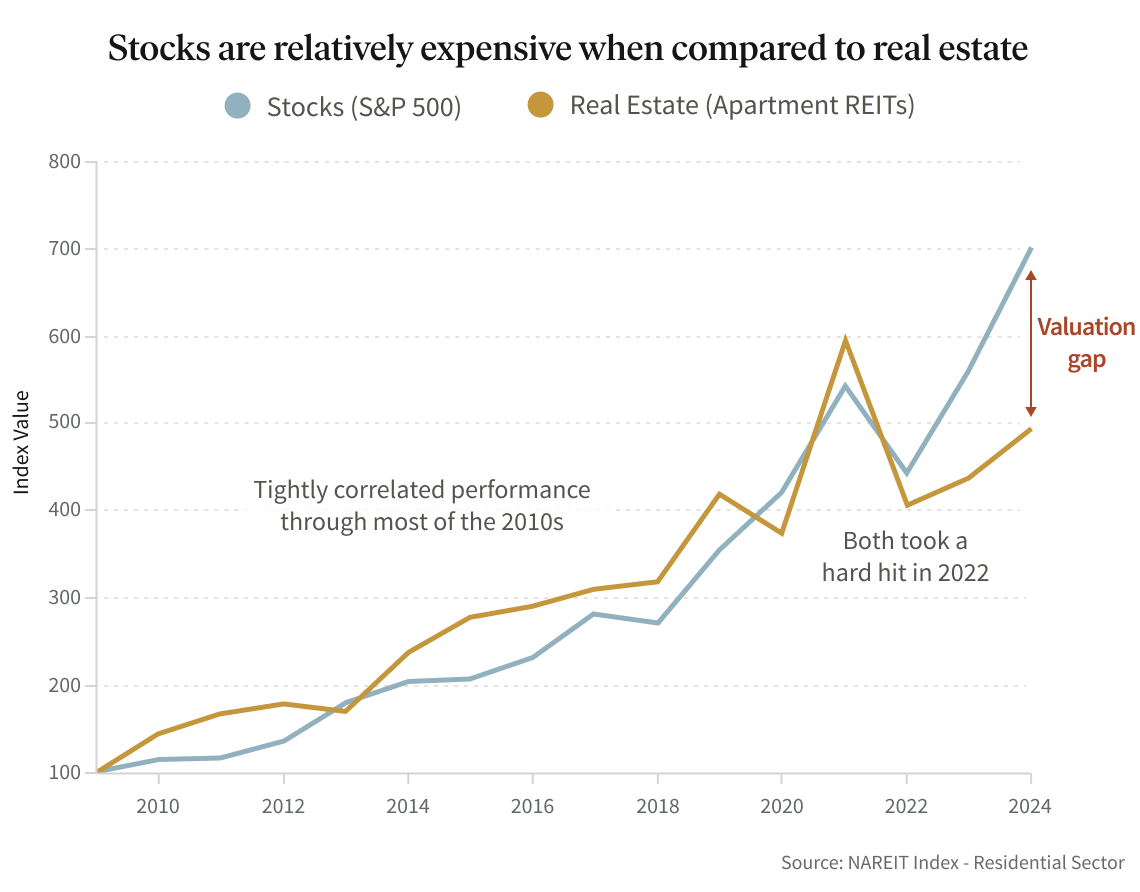

The valuation gap: Why asset allocation matters now

As Daniel Kahneman noted, rarely do we make decisions in a vacuum, instead we seek to make relative comparisons as a means to determine value.

This is true when it comes to investment. What constitutes a “good return” is more often a measure of relative performance rather than absolute. A 7% return may be underwhelming compared to 20%, but looks phenomenal when compared to -5%.

The stock market produced stellar returns over the past two years, recovering from the sharp decline in 2022 and once again hitting all-time highs. Meanwhile, real estate has yet to fully recover from the impact of higher interest rates, with prices still at a significant discount to their peaks in 2021.

What that means for investors is that stocks today are very expensive when looking at their price relative to future earnings. In fact, they are more expensive now than at most every point over the past 25+ years, except for the run-ups to the 2000, 2008, and 2021 bubbles, all of which preceded significant declines. (This relative overvaluation remains true despite sharp losses from tariffs over the past week.)

This relative pricing is the primary reason why many analysts, including those from top firms such as Goldman Sachs, have come out saying they expect stocks to return only 3% on average over the next ten years.

On the other hand, real estate looks relatively inexpensive. In almost direct contrast to stocks, many real estate assets are as inexpensive today as they have been at any point since shortly after the Great Financial Crisis (2009-2011).

As a result, we are seeing a growing number of professional investors and institutions starting to dramatically shift their portfolios out of public equities and into private markets.

The challenge for many individual investors is that this type of larger macro analysis is not something that is typically available to them (at least not on a regular basis). Instead, historical data suggests that individual investors are often the ones investing more as the market runs up and, in a dangerous game of hot potato, are then left holding the bag when larger corrections occur.

We believe investors that allocate a larger percentage of their portfolios to real estate and other private market assets will not only outperform but also benefit from greater stability as stocks become increasingly volatile.

Uncertainty begets volatility: Navigating a changing landscape

As we’ve stated previously, we don’t believe that mixing politics and investing results in us delivering better performance for our investors. However, we do recognize that we must be highly attuned to the ways in which dramatic policy shifts within the federal government may impact the economy, markets, and our portfolio.

Since the beginning of the year, uncertainty has replaced confidence as the prevailing sentiment in the market.

This is largely a reaction to the challenge of trying to forecast the potential impacts of the many recent policy changes, namely tariffs (and other protectionist policies), immigration (or lack thereof), a shrinking federal government (DOGE), and deregulation.

The new administration has been fairly explicit about their intentions to remake the global economic order by utilizing a tariff-driven approach not seen in more than 50 years (including adding new tariffs across nearly all trading partners).

They’ve also been fairly clear in their goals to bring down the national deficit by shrinking the size of the federal government and its corresponding budget, while also focusing on bringing down the interest rate on long-term treasuries.

Add to this the focus on curbing immigration and also deregulating a wide range of industries and you get one of the most broad-sweeping changes of policy instituted by any administration since the early 1980s.

In fact, even the administration itself has indicated they expect some short-term economic pain as the economy transitions to this new paradigm.

In the wake of so much uncertainty, it’s not hard to see why the market has become uneasy. And while the intent of the policies may be long-term benefit, as has occurred throughout history, near-term uneasiness and volatility can themselves lead to pullbacks that grow (unintentionally) into self-perpetuating downturns. In other words, regardless of the long-term impacts, we feel that in the near term it is prudent for investors to be positioned cautiously.

And while we remain fully aware of our limitations in being able to predict the broad-ranging impacts of all these policy changes, as we’ve stated before, we believe there’s strong reason to expect that at least in the near term they are beneficial to property values across the portfolio.

To summarize, we expect:

- Tariffs and uncertainty will likely slow economic growth, eventually leading to lower interest rates over the long-term which in turn would positively impact real estate values (We expect this to remain true despite near-term rising rates due to broader market dislocation)

- Reduced immigration and higher material costs will lead to increased construction costs and higher replacement costs for existing properties which reduces new supply and thereby drives up rent growth and property values

- Financial deregulation will likely reduce borrowing costs and increase credit availability, further driving up property values in the near term

Looking ahead: Positioning for continued success

We expect that over the next several quarters uncertainty and volatility in the stock market will only increase.

And while we cannot say with certainty that the elusive recession we had been forecasting since late 2022 will ultimately materialize, it does seem that the pressure from higher rates over the past several years combined with new tariff-driven headwinds are likely to slow growth in the U.S. substantially.

As a growing number of institutions and professional investors rotate out of stocks and into private assets, we will work hard to put our Fundrise investors into a similarly defensive position, aiming to shield the portfolio from the risks associated with broader volatility.

Fortunately, we believe the Fundrise portfolio will be in the enviable position of benefitting from both the same long-term secular drivers that have been our focus for many years, along with the near-term second and third-order consequences of the new administration's ongoing policy shifts.

As always, we greatly appreciate the trust that our investors have placed in us, and welcome any feedback or questions.

Onward.

| INVEST NOW |