The hard part is over… for real estate.

Our 2023 year-end letter to investors.

Key takeaway:

- Rising interest rates dragged down real estate returns throughout the year; fortunately, we believe the hard part is over and falling rates should, conversely, result in stronger performance for real estate investors going forward.

The past twelve months have proven to be the single most challenging year for real estate returns since the 2008 Great Financial Crisis, with nearly every property type experiencing negative performance, including a significant portion of the Fundrise portfolio.

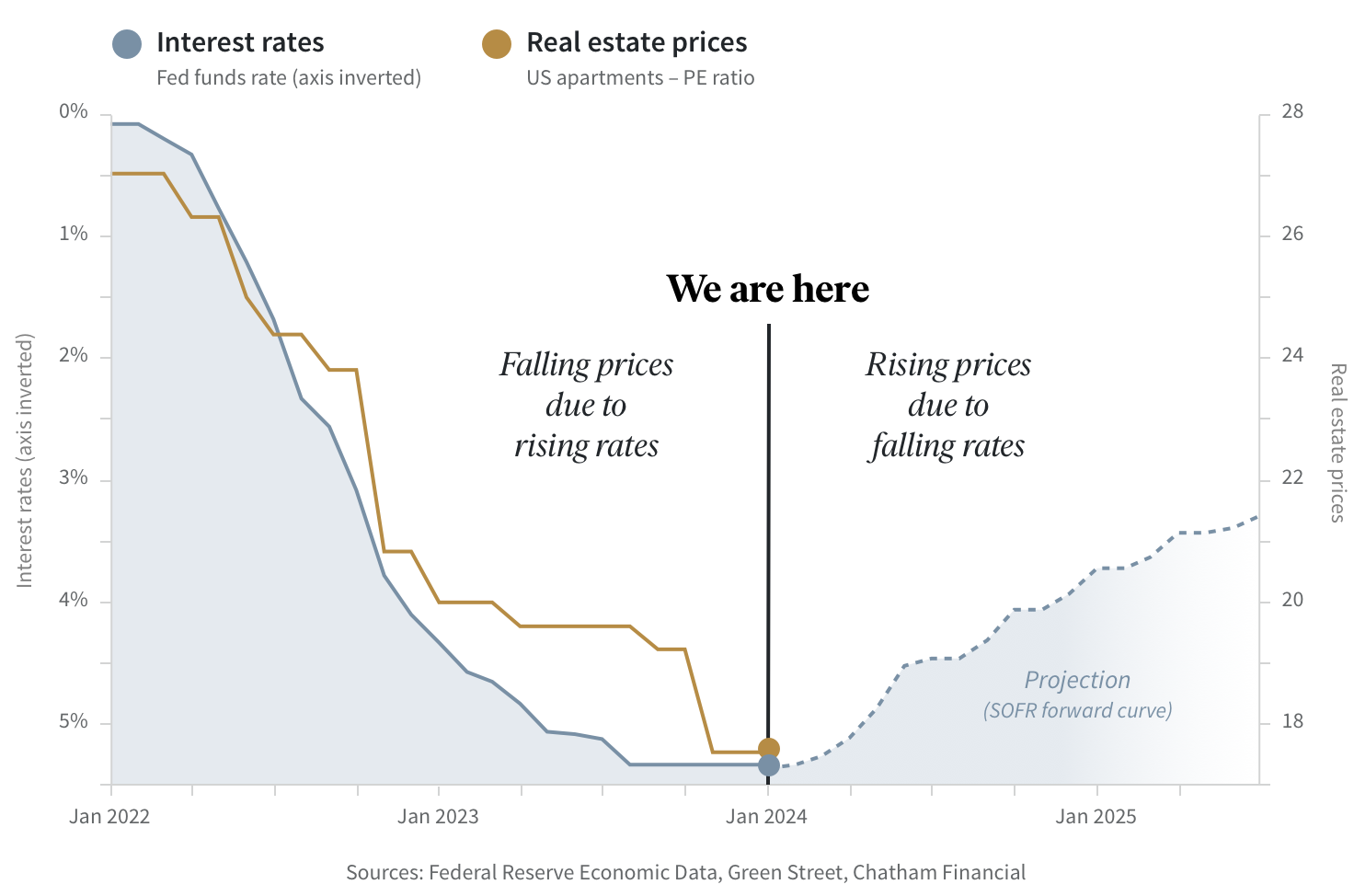

Fortunately, we believe we’ve reached a turning point with inflation now easing and the Federal Reserve signaling an end to rate hikes. As a result, we feel optimistic enough to call a bottom and state that we believe the hard part is over…at least for real estate investors.

Looking ahead, we believe that just as rising interest rates pulled real estate values down, falling interest rates will act as a strong tailwind, likely pushing real estate values higher and in turn producing potentially positive results for investors going forward.

Interest rate futures signal a rebound for real estate

What everyone got wrong

At the beginning of the year 100% of economists surveyed by Bloomberg predicted there would be a recession in 2023. Likewise, we were very much in agreement with this thinking, believing that the financial markets could not survive the fastest rate hiking cycle in modern history without eventually breaking in some form or fashion.

However, upon deeper analysis (shared at length in our mid-year letter) we concluded that the lag between the rate hiking cycle and a potential broader market downturn may take much longer than we’d initially expected, with historical data suggesting that such an event on average would be more likely to occur in the middle to end of 2024 (about 8-12 months after the Fed’s last rate increase).

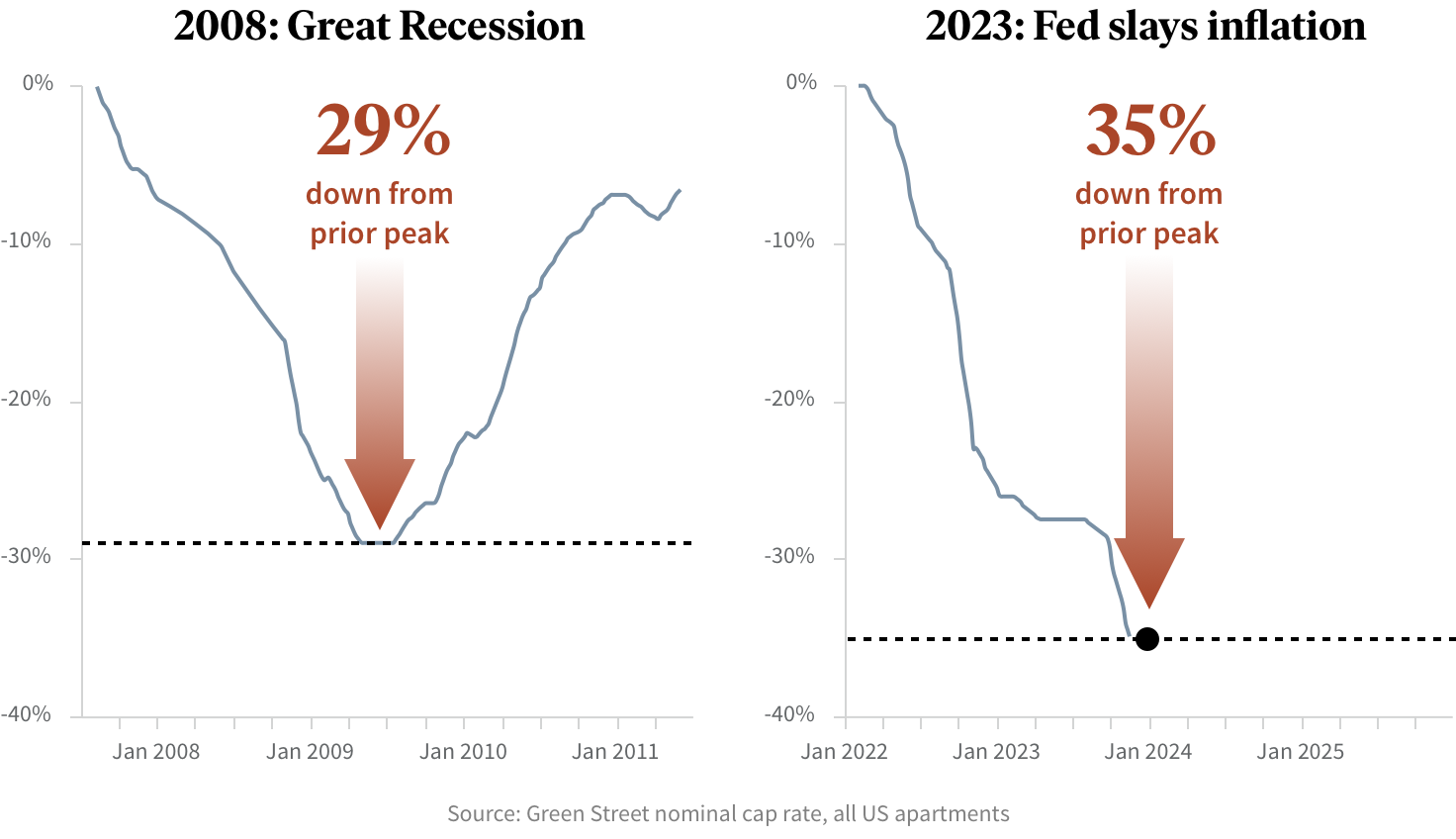

And while there was no broader recession in 2023, what many investors may not realize is that there was, in fact, a substantial recession across nearly the entire real estate industry with values in many cases falling between 20-40%, equal to or in some instances greater than the declines that were witnessed in 2008.

Lessons from history…

Apartment prices have fallen further than they did during the Great Recession

Again, we expect the transition to falling rates should bring about a reversal of this trend. It’s also worth noting that, for the most part, the single family for-sale housing market has been a notable exception to these types of declines in value.

You can’t fight the Fed

While we often talk about the importance of long-term fundamentals in driving returns, it’s equally true that in the short-term nothing is more impactful on asset values, and particularly real estate asset values, than interest rates.

Rising interest rates work like gravity pulling down real estate values regardless of the underlying fundamentals. (As we’ve noted previously, the standard operating metrics of property level health: occupancy, delinquency, rent growth, renewal rates, etc… all continue to hold up well across the portfolio despite continued downward pressure on the economy).

It was, therefore, nearly a foregone conclusion that, if the Fed continued to raise rates in 2023, real estate values (of all kinds) would fall by some measure over the course of the year. This reality was the primary reason that we began pulling back on new asset acquisitions as early as March 2022 and came into the year with nearly 25% of the entire portfolio being held in cash and undrawn credit lines.

Of course, in hindsight, even that large of a cash position was not sufficient enough to shelter the portfolio from experiencing meaningful markdowns. Looking back now, it’s clear that in order to completely prevent any negative performance, the portfolio would have had to have been 100% in cash as early as January of 2022 when the Fed Funds rate was still 0%.

Put more simply, nearly all investment real estate (that is real estate held as an investment asset as opposed to single-family home owners) saw a decline in appraised value due to the Fed raising interest rates.

When downturns are an opportunity

The benefit of being a long-term investor is that these kinds of markdowns are only on paper…unless, of course, you are either forced to or choose to sell prematurely.

The very same dynamics that lead to markdowns (on paper) also drive real buying opportunities for those who are able to capture them, a phenomenon we all witnessed in the stock market this past year.

Similarly, in the midst of the 2008 financial crisis, many people looked at their 401(k)s or home values in despair as they saw their “on paper” net worth fall by 30, 40, or even 50% in only a matter of months. In hindsight, however, many of those same people now look back on that period as perhaps the best investment opportunity of their lifetime and are kicking themselves for not buying at the bottom.

As our friends Michael Batnick and Ben Carlson from Animal Spirits have said previously, long-term investors, especially younger investors earlier in their careers, should actually hope for downturns and market crashes. Why? Because effectively, they are like a Black Friday event for the investment industry where great assets go on sale for prices that you otherwise could only dream about.

But knowing that is true and acting on it are two very different things. Most investors who bought a house in 2021 or 2022 would not today be willing to even entertain the idea of selling it for 20% less. They would say to themselves that such pricing was temporary and driven by higher mortgage rates, and that by simply waiting for rates to come down they would once again recover that value, and then some.

Yet that is exactly what many people end up doing with their investments, whether it be stocks or their Fundrise portfolio. As prices fall as a result of higher rates, they look at those negative returns (on paper) and turn them into real losses by selling or redeeming.

Again, knowing what to do and actually doing it are two very different things.

It’s the big things that matter

We live in a world that demands a constant stream of new and interesting content to digest. Financial news sites like CNBC or Bloomberg update articles multiple times a day with theories and predictions about why things are moving in one direction or the other. And, as a result, we are prone to over extrapolating a lot of the noise caused by “little things” that eventually just fade away into the background.

Ultimately, it’s the few big things (more obvious often than we’d like to admit) that really matter.

The past several years have seemingly been a steady stream of one random unprecedented event after the next, when in actuality they are the logical and sequential consequences brought about by the pandemic—it was the big thing.

The onset of covid led to a global shutdown. The shutdown broke supply chains along with decades old patterns and systems that had become ossified within both society and the economy. The response to the shutdown was unprecedented government stimulus, vast amounts of newly printed money, and a 0% interest rate monetary policy. This simultaneous shrinking of supply with a rapid expansion of demand led to inflation, which in turn led to the first significant rate hiking cycle in nearly 50 years. And rising interest rates led to a fall in asset values because, as we’ve now stated ad nauseam, prices move down when interest rates go up.

As the system continues to work through the domino effect of unwinding the past several years, we still expect tighter monetary policy to result in an inevitable dampening of the broader economy, including slower growth, rising unemployment, and potentially a significant decline in stocks. The irony is that in some sense regardless of the reason rates come down—either because the Fed was right about a soft landing or we are correct about a recession—it’s strongly positive for real estate values and, in our expectation, the Fundrise portfolio (again, remember that in the near term lower interest rates boost real estate values).

As we shift to this next phase of the Fed lowering rates, we expect there to be significant opportunities that will present themselves, which is why we plan to follow up over the next several weeks with a part two of this letter titled: It’s time to buy.

In the meantime, we again want to thank our investors for holding through the hard part. As always, we’ll continue to strive to be the tortoise among the hares. And, as usual, welcome your feedback and/or questions.

Onward.

P.S. For investors looking for a more in depth discussion on this topic, we encourage you to listen to the latest episode of the Onward podcast, entitled “Buying the Bottom", where we dive into the market dynamics driving the discounts in private real estate and the window of opportunity that exists as a result.

Appendices

Exhibit A: 2023 net returns of all client accounts of Fundrise Advisors by fund objective1:

| Fund objective | Net return |

|---|---|

| Income | 7.57% |

| Balanced | -11.93% |

| Growth | -7.89% |

| Overall | -7.45% |

Exhibit B: 2023 net returns of all client accounts of Fundrise Advisors by fund2:

| Fund name / Objective | Average principal3 | Launch date | Net return |

|---|---|---|---|

| Registered Funds | |||

| Flagship Real Estate Fund | $1,377,800,501 | Jan 2021 | -12.01% |

| Income Real Estate Fund | $550,054,182 | Apr 2022 | 7.57% |

| Innovation Fund | $86,657,949 | Jul 2022 | 1.60% |

| Growth | |||

| Growth eREIT | $249,040,905 | Feb 2016 | -6.11% |

| Growth eREIT II | $158,745,112 | Sep 2018 | -8.21% |

| Development eREIT | $129,322,918 | Jun 2019 | -9.73% |

| eFund | $94,194,543 | Jun 2017 | -2.71% |

| Growth eREIT III | $62,244,541 | Feb 2019 | -13.05% |

| Growth eREIT VII | $81,936,727 | Jan 2021 | -11.79% |

| Balanced | |||

| East Coast eREIT | $162,349,834 | Oct 2016 | -19.02% |

| Heartland eREIT | $91,770,698 | Oct 2016 | -7.46% |

| West Coast eREIT | $86,700,667 | Oct 2016 | -0.96% |

| Balanced eREIT II | $53,099,373 | Jan 2021 | -13.74% |