The Fundrise Opportunity Fund has continued to make strong progress through the first half of 2022 with several new leases signed and permitting and construction continuing to move forward. Additionally, despite increased market volatility and broader uncertainty as a result of rising interest rates, the portfolio has continued to hold its value, positioning itself for future growth as projects move through the development cycle and into stabilization.

Mixed-Use Developments

We ended our Q3 2021 update by mentioning the growing interest our projects were garnering from various media productions companies, with well-known names such as Stink Films and Mother both recently signing leases in our neighboring non-Opportunity Fund properties. To that end, we’re excited to share that interest has translated into another lease signed at the fund’s second mixed-use project with Somesuch, a now Academy Award-winning production company. Somesuch has signed a 12-year lease and is expected to move into their space after construction is completed next year.

We’re also excited to announce that we just recently signed a second new lease with a Michelin star restaurateur who will be bringing one of her award-winning concepts to the neighborhood. While we cannot share the specific details at this time, as we've agreed to coordinate the press release efforts with the tenant, we are extremely optimistic about what this kind of all-day neighborhood restaurant concept will do to bring further amenities and a balance of uses to the area.

In all, we view this continued leasing success (especially during a time when almost every major US city is seeing office and restaurant demand stagnate) as a monumental vote of confidence in both the area and the broader vision we have for sustainable growth in the corridor.

Office developments

Meanwhile, we remain on track with our ground-up creative office development and expect to receive our demolition permits later this year. While this type of large-scale urban development often takes years to complete (especially in this post-covid environment where permitting and approvals can take 2-3x longer), we’re continuing to work on scoping out the overall design of the project, including the parking plan, which stands to benefit both this property and neighboring properties. We expect this to help reinforce the long-term value of the properties given the extremely limited supply of parking in the area.

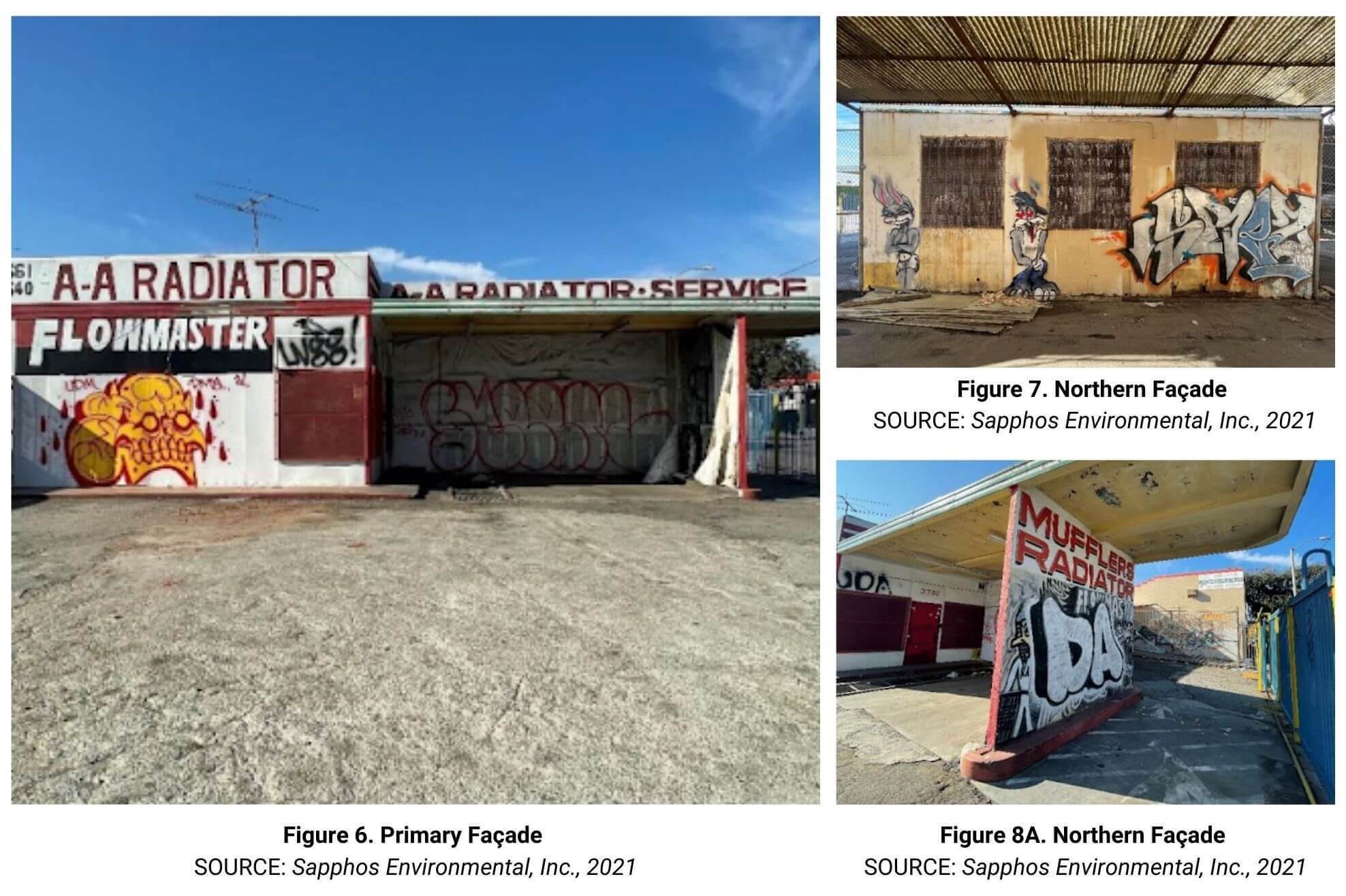

While progress is being made, these types of projects are not without their challenges. As just one example of the types of hurdles that exist in these types of development projects, we thought it was worth sharing one recent anecdote. As part of this large office redevelopment (see photos below) we will be replacing several older and functionally obsolete structures that are currently vacant, including an auto repair shop on the corner of the site. This of course falls within both the statute and spirit of the Opportunity Zone legislation aimed at creating significant investment in the physical improvement of older, out-of-use properties. During our permitting process, this repair shop site was flagged as potentially “historic” as it was once a gas station (likely 20+ years ago). If the city had determined the gas station is historic, it would have meant that we would be unable to remove the structure, despite it no longer being functionally operational as a gas station nor the broader area being in need of more gas stations, potentially making the project significantly less viable. We argued, successfully, that the site was neither historic in nature nor in good enough quality to actually salvage; however, the process of making this argument delayed the project by several months and, had it been deemed historic, it could have delayed things for several years. We share this not to complain but instead to shed light on just one of a number of similar challenges and obstacles that must be overcome to successfully move forward with a project such as this.

Fund performance

The Fund made its first NAV declaration at the end of December 2021, as originally scheduled in the offering documents. As was in line with our expectations, the NAV remained stable at $10 per share. It is common for development-heavy funds to see a flat NAV or even a markdown in NAV during the early phases of permitting and construction as costs are incurred but major valuation milestones have not yet been reached. For more information and examples of this, see this post on understanding the J-curve return nature of development investments.

Again, it’s worth reiterating that the fund is still early in its 10-year life cycle and given the long-term nature of the Opportunity Zone tax incentive structure, this fund, in particular, has deployed strategies that intend to take advantage of that feature but as a result, are likely to show less near term performance.

Looking ahead

Although many of the headwinds brought on by the pandemic have subsided, we expect to encounter continued delays due to both materials and labor shortages as well as longer permitting timelines. And while we still don’t expect these delays to have a substantial impact on the Fund’s long-term potential performance, we do anticipate that some of our original development timelines will be pushed back. All that said, we’re continuing to invest significant time and energy to find additional ways to advance our business plans faster and expedite the buildout process where possible. We look forward to sharing more with you over the next several quarters.