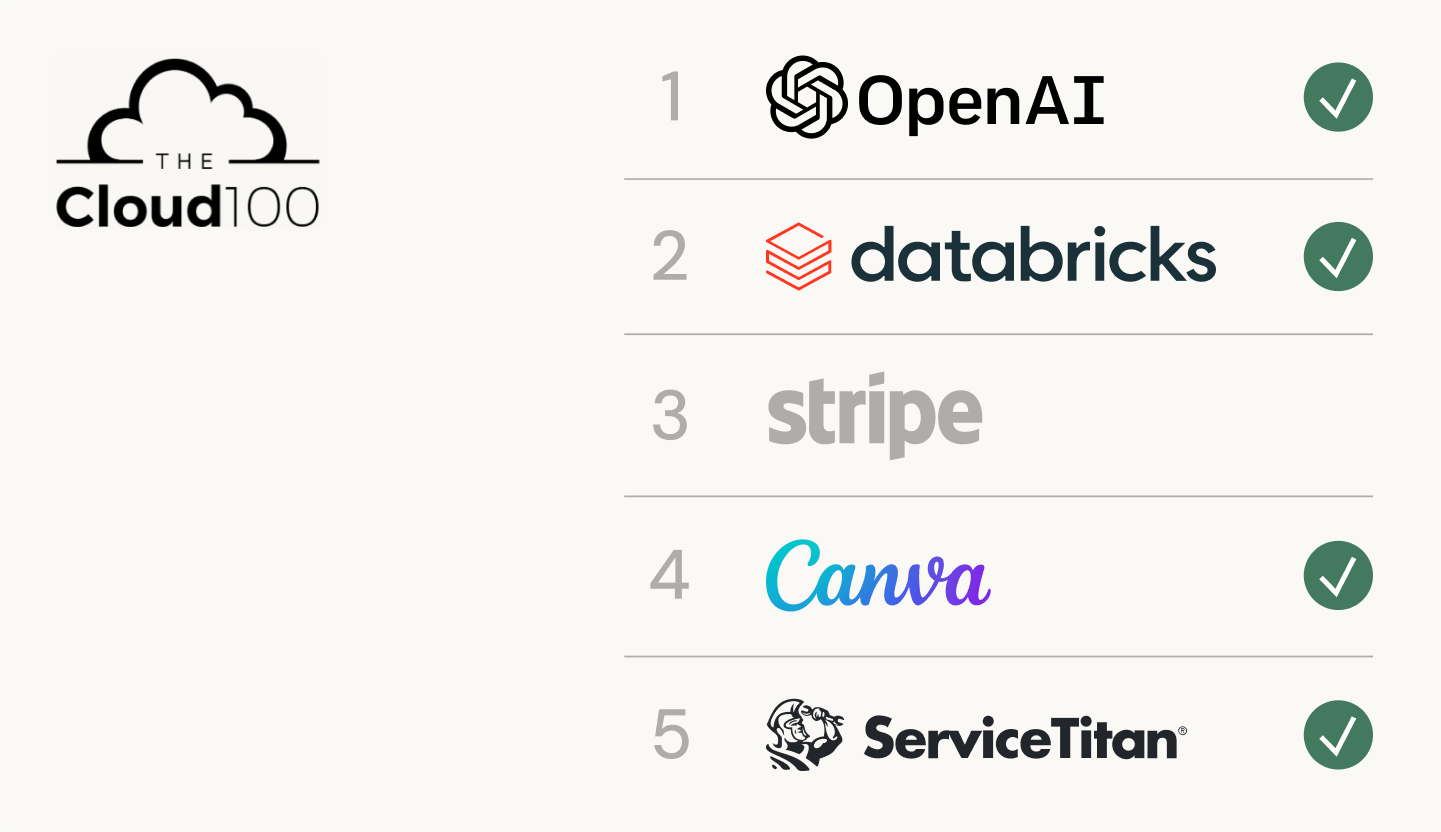

After its first full year of operations, the Fundrise Innovation Fund has achieved what many of its initial skeptics believed to be impossible — successfully investing more than $100 million into over a dozen of the top private technology companies in the world, including 7 companies on the Forbes/Bessemer Top 100 Cloud Companies Rankings — and 4 of the top 5!

The portfolio includes AI pioneers OpenAI, Anthropic, and Anyscale, among others. Data infrastructure leaders Databricks and dbt Labs. Two of the largest private companies in the world, Canva and ServiceTitan. As well as Vanta, one of the fastest growing SaaS security software companies, and Anduril, arguably the most exciting and innovative company in the defense industry.

It is not an exaggeration to say the portfolio, as it exists today, exceeds even our most optimistic initial expectations and that, in our opinion, it rivals the portfolio of any major active venture or growth fund that we are aware of. (We’d certainly welcome the feedback from any of our investors in the venture or tech industry as to what current fund has a more attractive percentage of its portfolio in winning companies).

Fundrise Portfolio of Top Companies in the World

Ranked by the Forbes / Bessemer Cloud 100

Democratizing venture capital by finding new opportunities

When we initially launched the Fund, we were certainly met with our fair share of skepticism, much of it from those within the venture industry who believed (or at least espoused) that no outsider could replicate their secrets to success. But we also heard doubt from some of the existing Fundrise investor base who expressed their concerns that our expertise lay in the real estate industry and that we were potentially getting too far outside our lane when it came to venture capital.

And to be fair, we welcomed that critique. Like our core Fundrise investors, we appreciate a skeptic and enjoy defying the status quo.

Still we were confident that the key to producing strong venture returns lay not in possessing some god-gifted ability to predict the future but instead in good old fashioned hustle, putting in the work to get in front of the best companies and then having the ability and the reputation to convince them that we could be valuable partners. As founders ourselves who’ve spent the past decade building our own successful technology company, we felt strongly that we could relate to their challenges and understood what they actually wanted.

We were also lucky. We launched the Innovation Fund in late 2022 just as the market started to shift and valuations for most tech companies were falling rapidly. There was an enormous amount of uncertainty and sentiment had become deeply negative. This allowed us to lean in while most others in the venture world were leaning out.

However, with uncertainty high and valuations falling the market for new venture rounds was essentially frozen. The best companies had more than enough money on their balance sheets and therefore did not need to raise any additional capital.

At the same time the IPO market had completely shut down, creating a challenge for those investors/ shareholders who had been assuming a relatively near-term exit. In many instances these groups either wanted (or needed) liquidity in order to fund other requirements or satisfy their own LPs. Either way, their needs created our opportunity.

We were early to recognize this trend and began aggressively pursuing secondary opportunities through a variety of different channels. And while we did participate in a number of primaries, our foresight around secondaries allowed us to get into arguably some of the best companies in the world at incredibly attractive valuations.

It’s also worth noting that getting the companies to actually approve the transfers (buying the shares from existing investors) is arguably just as big a challenge as finding the shares in the first place. As noted earlier, the best companies in the world have their pick of who they let on their cap table and we had to work hard to build confidence with the founders and executive teams that we would be a quality investor and long-term partner.

Part of the formula that succeeded was the unique nature of the Innovation Fund. Most of the companies already knew Fundrise either as a current customer of their products (e.g., dbt Labs) or because many of their employees were also Fundrise investors!

It also didn’t hurt that we could distribute their product to the 2-million-strong Fundrise user base — a decent sales and marketing value-add.

What does it mean to be one of the best private companies in the world?

For those of our investors that come from the tech industry the names of these companies alone likely speak for themselves, most are considered to be among the top tier of truly world class private companies.

However, for those of our investors who do not spend their day-to-day in tech, it’s helpful to look at the strength of the portfolio from a fundamentals point of view.

While a slight oversimplification, a decent rule of thumb when it comes to technology investing is that the first two indicators you want to look for are: 1) rate of growth and 2) scale of revenue. In other words companies that are capable of growing fast while producing large volumes of revenue tend to also have strong management, a winning product, and meaningful competitive advantages — which in turn tends to lead to strong returns over the long-term. Of course, over time, companies must show that they can not only grow revenue quickly but also do so efficiently, meaning they can produce profits. In fact, it is fairly easy to filter out excessive burn rates when we do our due diligence.

Again, contrary to the popular narrative, we believe identifying the best companies is fairly straightforward because the best companies have extraordinarily good metrics, especially at the more mature stages of investment.

So, in terms of revenue and growth rate, how does the Innovation Fund portfolio stack up?

When looking at the Fund’s portfolio of 14 private companies, the weighted-average annual company revenue based on the latest available reporting is roughly $1B while the average annual growth rate is an astonishing 374%.

Even when excluding the large AI LLM companies (which have shown themselves to have an unusually high growth rate even for technology startups), the remaining portfolio of 11 companies has a weighted-average annual revenue of roughly $1.1B with an average annual growth rate of 87%.

For reference, the Nasdaq 100 grew revenue by 15% last year, while the S&P 500 grew revenue by 4%.

Said another way, the portfolio consists of companies that are producing exceptionally robust revenue at an exceptionally high growth rate, and you’d be hard pressed to find a diversified private portfolio of any material scale that would exceed these numbers.

| Key Metrics of the Private Tech Company Portfolio | ||

|---|---|---|

| Stage | Revenue scale weighted average |

Growth rate weighted average |

| Early & Mid Stage 6 companies / 10% of private company portfolio |

$13 million | 135% |

| Late Stage 4 companies / 32% of private company portfolio |

$186 million | 625% |

| Pre-IPO 4 companies / 58% of private company portfolio |

$1.6 billion | 338% |

| Total Private Company Portfolio 14 companies / 100% of private company portfolio |

$1 billion | 374% |

| Total, excluding AI companies 11 companies / 86% of portfolio |

$1.1 billion | 87% |

Note, part of the portfolio strategy is to hold a percentage of the fund invested in liquid assets, which today are held in cash and bonds. The liquidity is critical to meet potential quarterly redemptions and to have dry powder available to write large checks for additional private investments.

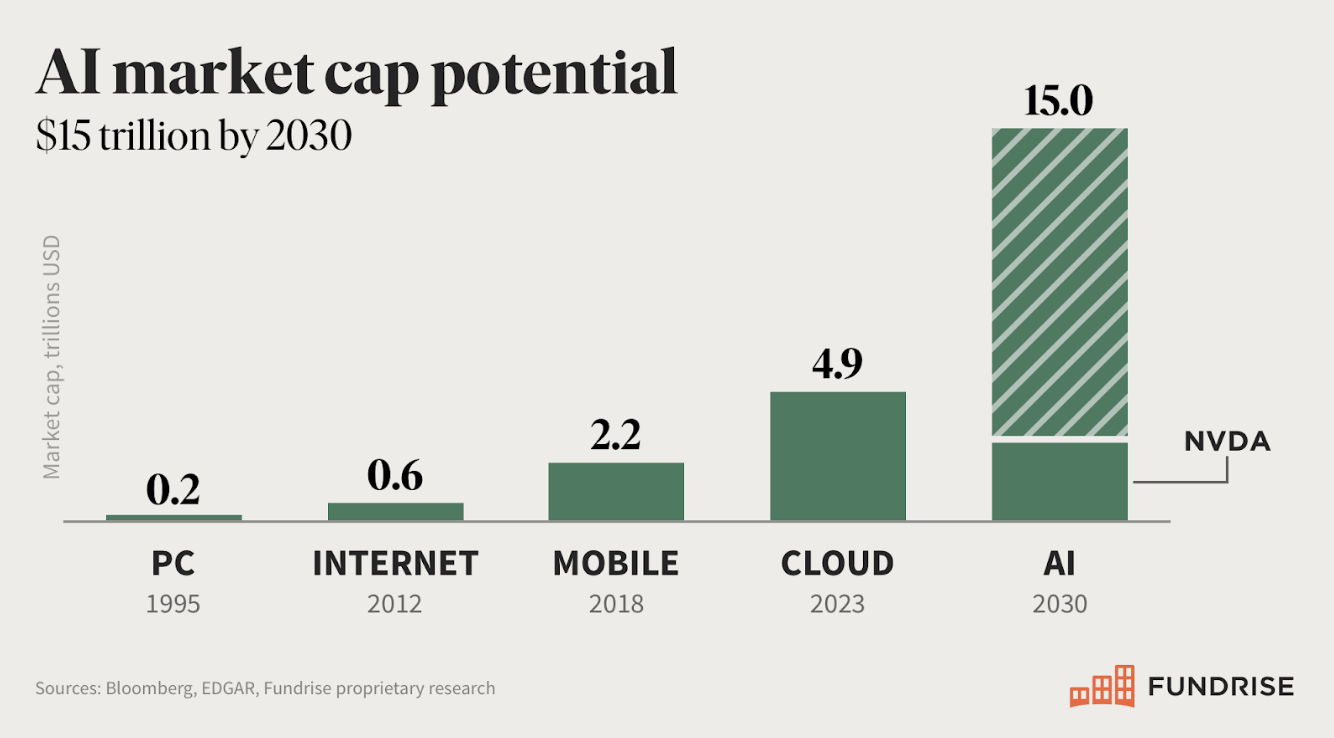

Catching the AI wave

Shortly after launching the Fund, OpenAI released its first version of ChatGPT in what will likely go down as the seminal moment in AI and also illustrating once more that it’s better to be lucky than smart. We’ve stated before that we believe AI is a fundamental technology shift on the same order of magnitude as the internet or potentially even (as provocative as it sounds) electricity. It is not only birthing new products, companies, and sectors but is starting to amplify the growth rates of nearly all businesses and industries that are adopting it.

We are currently working on publishing an in-depth analysis of AI’s market potential which we plan to share with you all soon, but suffice it to say that the growth of AI has materially changed the landscape for technology and venture investing and we expect it will continue to be a focal point for the Innovation Fund for the foreseeable future.

Looking ahead

As excited as we are about the Fund’s progress to date, we also know this is only the beginning of what ultimately will be a market revolution.

Already, we are seeing the broader trend of opening up access to venture capital gain more and more steam and just as was true with the 150 copycats we had in real estate over the past decade, we expect there will be an increasing number of companies claiming the narrative of “democratizing access” in an attempt to capture some of the excitement. Unfortunately, as was true for real estate, it will probably take several years (and some number of investors losing money) to separate the wheat from the chaff.

Ultimately, we believe the strength of the portfolio we’ve produced can serve as a stepping stone to further validate the Fund as an established investor for high growth companies. And that we’ll be able to continue to show an ability to drive sales and marketing value for our portfolio companies by leveraging the scale and collective power of the Fundrise investor base.

It’s also worth reminding all our investors that despite the exceptional quality of the existing portfolio, the Innovation Fund is a more illiquid investment than our real estate funds and is likely to experience greater volatility. Even on a long-term positive return trajectory, there will almost certainly be extended periods where valuations stay flat and some intermittent periods where values fluctuate dramatically both up and down. Those types of movements are intrinsic to the venture capital asset class and will be difficult, if not impossible, to avoid. We want to stress the importance of investors taking those realities into consideration as they choose to continue to invest going forward.

Overall, we could not be more excited about the position the Fund is in today. As we stated when we first launched, we believe venture capital is one of the most attractive asset classes and has arguably the best potential to produce outsized returns over the next several decades. With the advent of AI, this is more true than ever before. Opening access to the venture asset class therefore could not be more fundamental to the long term mission of Fundrise.

We look forward to continuing to push the new frontier with you.

Onward.