Summary

- During the transition phase of the economic cycle, we focus on buying credit.

- We have been opportunistically acquiring credit for the Innovation Fund as we wait for private tech markets to finish bottoming out.

- Credit has been very attractively priced which we illustrate with some examples.

The Innovation Fund’s main objective is to invest in private tech markets. Some investors may then wonder why we have deployed a portion of the portfolio in credit. Although debt of tech companies’ is not the primary focus of the Innovation Fund, when the market presents extraordinary opportunities, we are generally of the view to accept them.

Private tech company valuations have been slow to come down from the prior lofty multiples. Longtime Fundrise investors know that we prefer a deliberate approach (i.e., the tortoise over the hare). We expect the wider market to take one more leg down later this year as the economy enters a recession. For this reason, we have been focused on investments in debt while we bide our time waiting for a full market reset. In the meantime, we have been purchasing bonds of public tech companies, which can generate equity-like returns during periods of market dislocation.

An illustration is worth a thousand words

To understand the credit strategy, we thought it would be helpful to illustrate the potential returns with an example.

Earlier this year, we purchased bonds of Match Group, a $15.0 billion public company that owns Match.com, Tinder, OKCupid, and many other online dating brands. Match Group has over $3 billion of annual revenue and trades at 4.75x revenue or 38x earnings per share (P/E).

We purchased the bonds of Match Group at a 7.49% yield-to-maturity. Obviously, bonds of billion-dollar, publicly-traded tech companies are much lower risk than the equity of private startups.

Because of the lower risk, banks will lend against the asset. In this instance, one of our banks offered terms of a 75% advance at 1.3% above overnight rates, which based on the forward curve is approximately equivalent to an average 4.8% interest rate over the 6-year life of the Match Group bond.1

If we were to lever the Match Group bonds at these lending terms, the result would generate a 15.5% current gross yield, which seems pretty attractive, in our opinion, especially on a risk-adjusted basis.

| Principal | Yield-to- Maturity |

Yield | Gross Yield | Approx. Net Yield |

|

|---|---|---|---|---|---|

| Match Group | $1,000,000 | 7.49% | $74,900 | ||

| Loan | $750,000 | 4.80% | $36,000 | ||

| $250,000 | $38,900 | 15.56% | 13.31% |

However, purchasing corporate bonds is not as simple as it sounds. The bond market is much more opaque than stock markets. Bonds are bought over the counter, e.g., through a Bloomberg terminal, and your broker is often trading against you. Frequently, the bonds we targeted would only trade once every few weeks and were typically denominated in the millions of dollars.

We have not yet borrowed against the bond portfolio because we believe there will be significant volatility through the later half of this year. Plus, it almost goes without saying that it is critically important to manage the many risks of leverage.

The main point we are trying to illustrate with the above analysis is the attractiveness of credit markets.

Corporate bonds

Below is the Innovation Fund’s corporate bond holdings as of mid- June including an estimated levered yield based on the provided lending terms:

| Company | Market Cap | Maturity | Price | YTW | Face | Principal |

|---|---|---|---|---|---|---|

| Roblox | $24.0B | May 2030 | $83.11 | 6.88% | $3,500,000 | $2,908,520 |

| ZoomInfo | $9.1B | Feb 2029 | $86.78 | 6.58% | $3,000,000 | $2,603,380 |

| Twilio | $8.7B | Mar 2029 | $85.15 | 6.60% | $2,000,000 | $1,703,060 |

| Twilio | $8.7B | Mar 2031 | $82.25 | 6.78% | $1,000,000 | $822,500 |

| Elastic | $5.8B | Jul 2029 | $85.25 | 7.03% | $2,250,000 | $1,917,020 |

| Block | $33.6B | Jun 2026 | $88.63 | 6.67% | $1,000,000 | $886,250 |

| Block | $33.6B | Jun 2031 | $80.88 | 6.54% | $2,000,000 | $1,617,500 |

| Uber | $75.8B | Jan 2028 | $97.57 | 6.84% | $1,000,000 | $975,680 |

| Match | $8.8B | Feb 2029 | $91.15 | 7.49% | $1,000,000 | $911,500 |

| YTW | Principal | Yield | Gross Yield | Net Yield | ||

|---|---|---|---|---|---|---|

| Bond Portfolio | 6.79% | $14,345,410 | $974,053 | |||

| Loan | 4.80% | $10,759,058 | $516,435 | |||

| $3,586,352 | $457,618 | 12.76% | 10.51% |

Later this year, we intend to lever the bond portfolio, which should boost fund yields and play a useful role in the overall portfolio strategy.

Busted convertibles

We also pursued a similar strategy with convertible debt. The primary difference is that convertible bonds have the ability to convert to equity at a predetermined price, which can be accretive in two main circumstances.

In normal times, convertible debt offers the option to convert at a discount to an expected future share price, with the assumption that the company is likely to continue to grow. For instance, in 2021 Cloudflare issued convertible bonds at a 0% coupon with the option to convert at $191 share price in 2026. Typically, the result is the convertible bond offers a comparable upside as equity but with limited downside since it is debt.

However, when valuation multiples collapsed last year, most of the pre-set stock prices were so far off from current prices that the convertible bonds started trading mainly on yield, which is why they are called “busted convertibles.” For instance, Unity Software’s convertible debt was originally issued at a 0% interest rate. When it started trading on yield instead of as a potential conversion to equity, we purchased it at a 6.84% effective interest rate, which as we illustrated above we can lever into about a 10.5% net yield.

Below is the Innovation Fund’s convertible bond holdings as of mid-June:

| Company | Market Cap | Maturity | Price | YTW | Face | Principal |

|---|---|---|---|---|---|---|

| Unity Software | $10.6B | Nov 2026 | $77.68 | 6.84% | $2,000,000 | $1,553,500 |

| Confluent | $7.2B | Jan 2027 | $78.75 | 6.17% | $1,000,000 | $787,500 |

| Cloudflare | $17B | Aug 2026 | $84.63 | 5.16% | $1,000,000 | $846,250 |

| Splunk | $14.6B | Jun 2027 | $86.88 | 4.49% | $1,000,000 | $868,750 |

| Jamf | $2.0B | Sep 2026 | $83.63 | 5.32% | $1,000,000 | $836,250 |

In addition to the yield, there is a second, tantalizing reason why busted convertibles can be attractive. With valuations so much lower, some of these companies become acquisition targets. It is easy to imagine a private equity fund acquiring Jamf, which is trading at 4x revenue multiple.

If a company is acquired, the buyer must pay off our convertible debt. We purchased Jamf convertibles at $83.63. If the company is acquired, our bond must be redeemed at $100, which would generate an immediate gain of 16.37%, on top of the current yield.

Convertible debt investment performance can behave countercyclically because the more stock prices fall, the more attractive these companies become to potential buyers, increasing the likelihood of the bond getting redeemed at par (full value).

Looking ahead

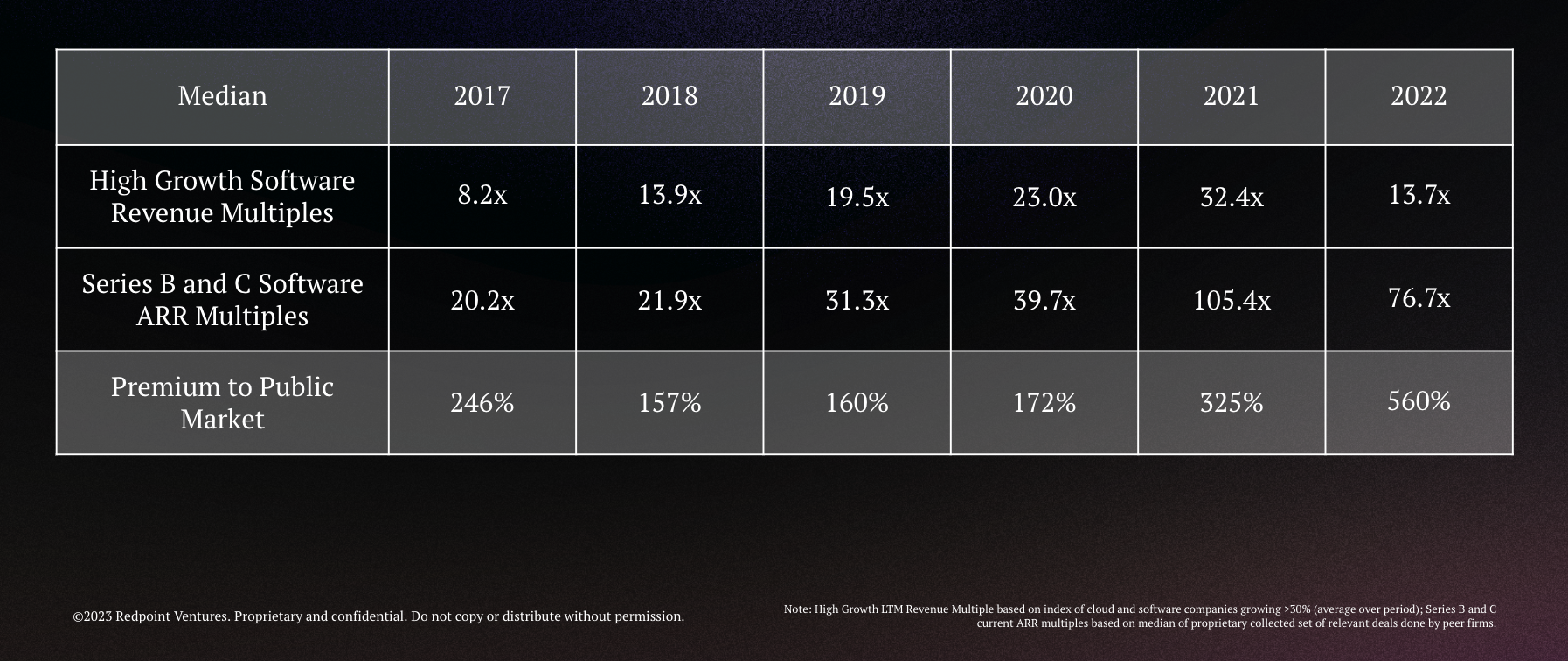

The primary focus of the Innovation Fund is to invest in pre-IPO tech companies. The challenge has been that private tech company valuations have a way to go before their prices return to historical norms.

Below is a table from the folks at Redpoint Ventures comparing revenue multiples of public software companies to private software startups.

As you can see, prices of private tech are likely to decline further before they become in line with public company metrics. Having said that, there are exceptions, as was the case with our investment in Vanta, which has gone from success to success over the past nine months.

As long-term fundamental investors, we have usually found patience is rewarded. In the meantime, we remain vigilant for additional market disruptions as high interest rates, the debt ceiling, and the ongoing banking crisis create opportunities for agile and liquid investors (as we did with the Silicon Valley Bank Rescue Program).

We appreciate your support and as always look forward to your questions and feedback.

Onward,

The Fundrise Team