The Capital Stack Explained

Often when you hear someone describe the financial structure of a real estate deal they will refer to the “capital stack” (frequently depicted as a bar graph or pyramid). The capital stack represents all the different types of capital invested into a real estate asset and the relationship between each category.

Traditionally, there are two main types of capital:

- Equity, which represents an ownership interest in the asset.

- Debt, a loan given to the equity ownership and typically collateralized by the asset itself or other assets of the equity owner.

Seniority and Risk

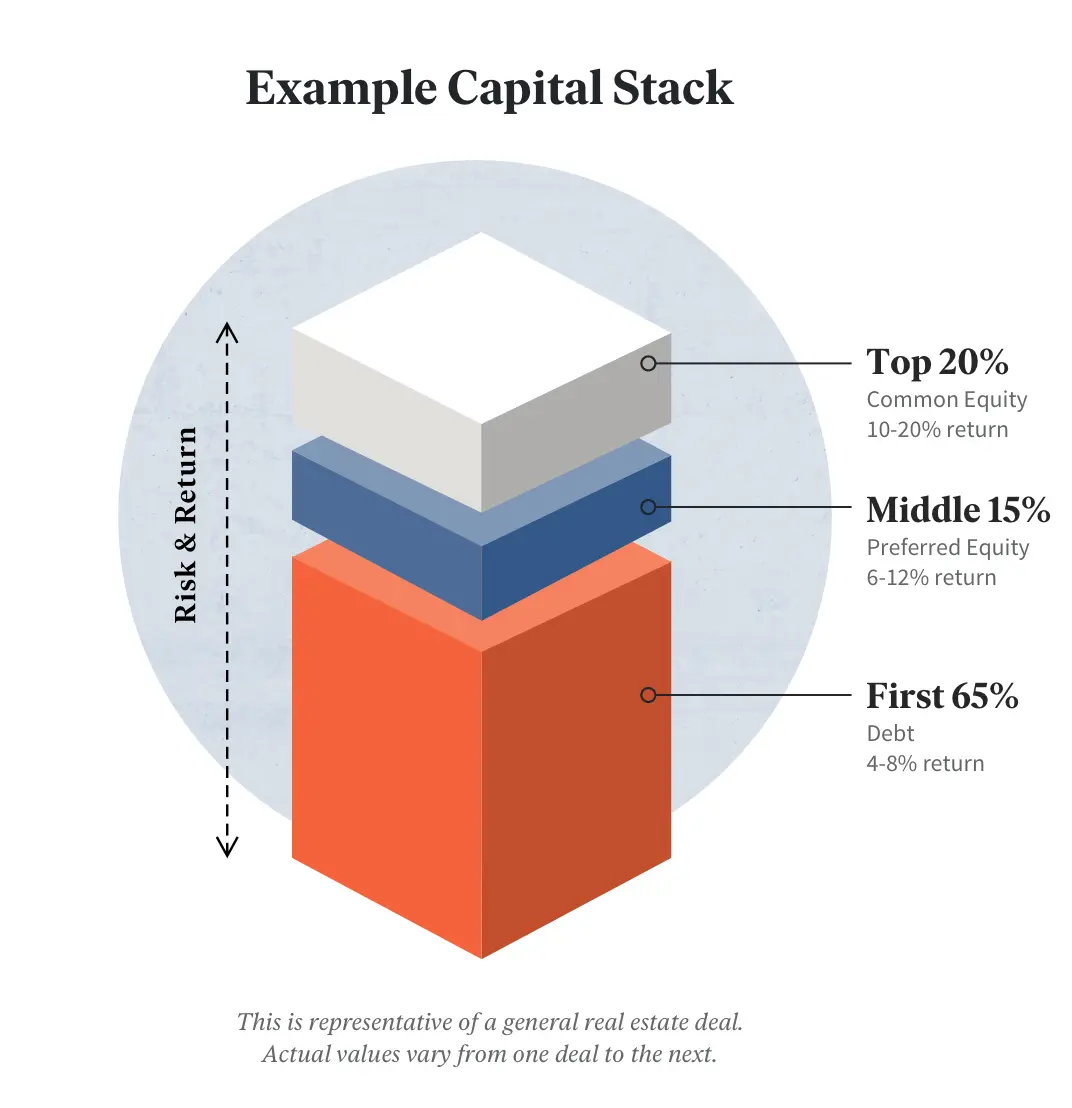

The capital stack outlines the relationship between the equity and the debt. The lower down on the stack the lower the risk to that capital, and vice versa as you move higher up. This lower risk then translates to a lower return. As you move up the stack, the risk and potential returns increase accordingly. This relationship can also be described as seniority.

Debt

Debt is always lower down on the capital stack and therefore senior to the equity, meaning that it is first to be paid back. Most real estate debt is provided by traditional lenders, such as banks, that take the senior secured position. Because senior debt is in the most secure position, the return (or interest rate) charged is the lowest and is often fixed or capped. Debt also comes with a fixed term, at the end of which the equity ownership must pay back the entire principal plus interest or risk losing control of the asset.

Equity

Equity owners are at the top of the capital stack and are in the riskiest position; they are last to be paid back. Because of this, equity investors typically require the largest returns to compensate for that risk. Equity investors, unlike debt, participate in the success of the investment, meaning that their upside or potential returns are not capped but can increase or decrease depending upon the performance of the investment. Because equity investors are owners of the asset there is no fixed term for the investment; full payout only occurs when the asset is sold or an individual investor sells his/her ownership interest.

In almost all real estate deals, there is a sponsor (often a manager or developer) that contributes a small portion of the equity and is responsible for the management and performance of the actual investment. The sponsor will raise additional equity from investors who take a senior position within the equity itself, frequently receiving a preferred return and first payback rights.

Preferred Equity

As financing for real estate deals has become more complex, there have been additional types of capital added to the stack that often act as a hybrid between equity and debt. This category is often referred to as mezzanine debt or preferred equity. As a hybrid structure, this type of investment is senior to traditional equity investment but subordinate to the debt. Often the return structure is also a hybrid between true equity or debt, where mezzanine/preferred equity investors receive a fixed annual payback over a specific investment term but potentially can participate in the upside or continued success of the investment.

Each real estate deal is unique, and the factors that contribute to the potential risks and returns vary. The structure of the capital stack will therefore also vary from deal to deal. As an investor, it is important to fully understand the potential risks at each point in the stack and also have a clear outline of exactly what returns you are entitled to. Not all investment structures are suitable for all investors, as with more complexity also comes more risk and the potential for a complete loss of an investment.