Outside voices: To understand the current crisis, look to calamities of the past

In this post, we asked Jamie Catherwood (author of the popular financial history blog Investor Amnesia) to show how the worst economic shocks of a crisis are actually a result of second or third-order ripple effects, which play out in unpredictable ways.

Editor’s note: We plan to occasionally feature top minds from outside Fundrise to explore topics that we feel provide insight and understanding on critical investment ideas in these turbulent times.

Interested in seeing more content like this? Please take a moment to share your feedback

——

While it sounds implausible after what’s unfolded in recent weeks, the S&P 500 hit six (six!) all-time highs in February, and as recently as Thursday, February 21. Just two trading days later on Monday the 24, though, everything shifted.

On that Monday the S&P 500 fell -3.3%, the Dow Jones Industrial Average dropped -3.6%, and the NASDAQ declined -3.7%. All three indices proceeded to enter bear markets, with the S&P 500 doing so at a record pace.

Since the lows, markets rebounded and the NASDAQ is actually positive year-to-date. However, the impact of COVID-19 is far from over, and investors should continue to position themselves for the future by consulting the lessons of history.

The unpredictable outbreak nature of this pandemic caught the whole world off guard and brought strong economies to their knees. Has an exogenous shock ever blindsided markets like this ever happened before?

Of course.

The catalyst

In his book A History of the United States in Five Crashes, Scott Nations argues that most crises are preceded by a catalyst, or ‘shock’, that initiates the downturn. These catalysts are largely unpredictable, but their impact on markets is certain. The catalyst may appear unrelated to financial markets, but the ripple effects quickly become waves that drown economies.

Today, coronavirus is the ultimate example of what a catalyst or ‘exogenous shock’ looks like. After soaring 30% in 2019 and the American economy appearing strong, there was ample reason to feel optimistic about US stocks heading into 2020. The 2020 forecasts from asset managers had largely painted rosy pictures, but these forecasts became utterly useless and outdated in a matter of weeks.

Even after news spread of the coronavirus outbreak in China, most could not begin to fathom what was on the horizon. With confirmed cases in 169 countries, it is still hard to grasp the toll this will have on global economies and populations. In terms of economic impact, however, the knock-on effects are emerging in places like the Airline, Dining, Hospitality, and Manufacturing industries. In fact, it's the unexpected domino effects that hit the economy hardest.

Boeing is a prime example of how quickly an exogenous shock like coronavirus can blindside the market. In short order, the most valuable industrial company in America, Boeing, sought a $60 billion bailout from the US government because of the steep decline in air travel.

A similar scenario is unfolding in the restaurant industry:

To try to understand the path forward we will consult the lessons of history provided by a catastrophic event from over a century ago.

The earthquake that moved markets

On the morning of April 18, 1906, at 5:13 AM, an earthquake registering 8.3 on the Richter scale tore through San Francisco. The earthquake itself only lasted 45-60 seconds, but was followed by massive fires that blazed for four days and nights, destroying entire sections of the city.1 Making matters worse, the earthquake ruptured the city’s water pipes, leaving firefighters helpless in fighting the flames.

Eventually, the earthquake and ensuing inferno destroyed 490 city blocks, some 25,000 buildings, forced 55–73% of the city’s population into homelessness, and killed almost 3,000 people. In a matter of days, the Pacific West trading hub looked like a war-torn European city in World War II.

Like coronavirus, the unpredictable nature of San Francisco’s earthquake made it all the more damaging, and had a domino effect in seemingly unrelated areas of the economy.

The market reacts

When news of the catastrophe spread, markets reacted immediately. In New York, the NYSE stocks plummeted roughly 12%. The below article from a newspaper published one day after the earthquake summarized Wall Street’s response:

Even San Francisco’s famous cable car system wasn’t spared, as the earthquake destroyed countless cable cars. United Railways Investment, the company operating the cable cars, saw its stock drop 30% in a day following news of the disaster.

Echo effects of the San Francisco earthquake

To understand how the impact of this earthquake spread, we must recognize the presence of Britain’s fire insurance industry in San Francisco. Historians Kerry Odell and Marc Weidenmier stated:

“Endowed with an excellent natural harbor and easy coastal and river access to the agricultural and natural resource riches of the west, San Francisco had developed strong economic ties to other countries, particularly to Britain. Most of the wheat exported from the west coast and bound for England was financed through San Francisco, and a sizable number of London banks had offices in that city. At the same time, other British financial institutions sought to expand their business in the area. Prominent among these were the British fire insurance companies.”2

In fact, the Liverpool & London & Globe fire insurance company opened San Francisco’s first fire insurance office in 1852.2 Britain’s presence continued expanding until “at least half of all fire insurance policies were issued by British companies” in 1900.2 This international link made a local problem global, causing an outbreak of second and third order consequences.

Insurance payouts and Britain’s gold exodus

While the San Francisco earthquake was a national tragedy, the knock-on effects had a much larger economic impact. In particular, insurance payouts from London to San Francisco transferred the impact of a localized natural disaster across the broader economy.

The 1906 earthquake was an insurance nightmare. On April 19, 1906 the Minneapolis Journal stated:

“The owners or property destroyed by earthquake cannot collect a dollar under their fire-insurance policies, even though the buildings that fell were later swept by flame…”

Incredibly, there was also not a single insurance policy written to “cover disasters by earthquakes”. So with thousands of homes damaged by the earthquake, but homeowners only holding fire insurance, who was liable for covering the damages? Well, according to the British fire insurance firms:

“The insured can only collect on a building fired while standing. Once a structure is shaken down by earthquake the writers of insurance on it are not liable.”

Since fire damages were covered, but earthquakes were not, desperate San Franciscans were incentivized to burn down their own houses, which they did. The table below shows the policies and estimated losses of British firms:

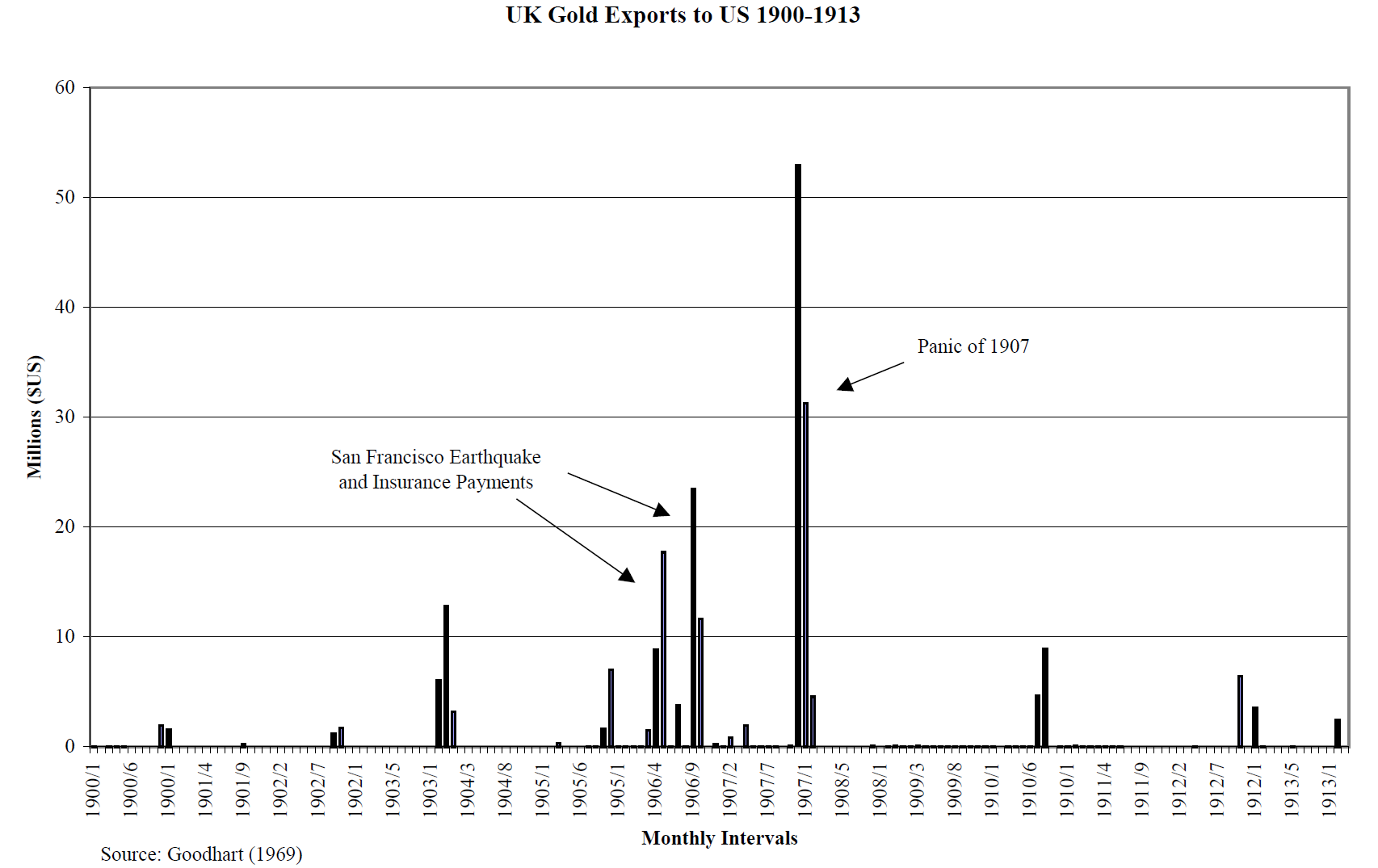

However, the impact of these payments were felt far beyond the balance sheets of these companies. The substantial payouts by British firms caused a mass outflow of gold from London as ships were loaded with gold bars for their transatlantic journey to San Francisco. By the end, Britain had outflows equal to 14% of its national gold reserves.2

“The San Francisco earthquake gave rise to a massive outflow of funds – of gold – from London. In total, quake related payments to the United States represented 40 percent of seasonally adjusted British gold exports for all of 1906… These flows were nearly two-and-half times more than British gold flows to any other country in 1906.” 2

Domestically, New York financial institutions were also hampered by depleted gold reserves from transfers to San Francisco. The New York Times stated “imposed a substantial drain upon the banks of [New York]”. 3

As the Bank of England’s (BOE) ratio of reserves to deposits hit a 16 year low, there was little choice but to raise interest rates to protect its gold reserves. In September and October of 1906 the BOE raised rates 250 bps to 6.0%, which one American paper called an unexpected “bombshell in the market”.

However, American investors held no confusion over why the BOE made this decision:

“The bank rate is now 6 per cent, the highest rate since the Baring failure sixteen years ago. This step was, of course necessitated by the impoverished condition of the Bank of England [gold] reserve…” 4

They also recognized the negative implications this had on the US market:

“The advance in the bank rate was undoubtedly in sheer self-defense… Its effect upon stock speculation must be unfavorable, and prices must fall more or less in consequence… It means that there is an end coming to reckless speculation, and that nothing but liquidation of greater or less severity can restore equilibrium…” 4

While raising rates to 6.0%, the BOE also practically forbid British firms from accepting American ‘finance bills’, which were “used to finance gold imports into the United States” and provide credit. This devastated firms in the United States, and New York in particular.

“This policy resulted in a significant fall in American securities markets, as the collateral for those bills was sold, and led to significant gold outflows from the United States. A relatively weak cotton harvest in 1907 resulted in low export revenues, further aggravating the stress on the banking system and financial markets.” 5

Remember, this all stemmed from the earthquake in April 1906. What started as a national disaster in San Francisco led to an outflow of gold in London. This forced the BOE to raise rates, which reduced American firms’ access to credit and depleted their gold reserves. This sparked widespread selling of stocks to raise cash as ‘finance bills’ came due for payment, and could not be renewed because of the BOE’s new policy.

The U.S. money market thus found itself “low on gold reserves and vulnerable to shocks”. 5

The final straw: Knickerbocker and the investment trusts

The final straw, however, was the rise of investment ‘trusts’ in New York. These trusts were financial institutions that took deposits but were less regulated than banks, and provided almost every single function outside of issuing notes. They were the ‘shadow banks’ of 1907. These trusts could buy/sell stocks and corporate debt, underwrite/distribute securities, receive deposits, and make loans.

Yet, despite all their similarities with banks, they were excluded from the New York Clearing House (NYCH), “a private organization that facilitated clearing and that could provide emergency lending to its members, as well as issue ‘clearing house certificates’ to serve as substitutes for currency in times of crisis.” In other words, investment trusts could not access the one institution able to throw them a lifeline in times of crisis. What made trusts even more fragile was the fact that the lightly-regulated trusts had no legally mandated reserve requirements like their bank counterparts.

So after a failed ‘corner’ in the copper market inadvertently led to a ‘run’ on the second largest trust in New York, the Knickerbocker Trust, the fragile markets were finally tested. The run on Knickerbocker followed the National Bank of Commerce’s announcement that it would not serve as Knickerbocker’s clearing agent. Again, because of the trust’s low ratio of cash reserves to deposits, they were particularly exposed and “vulnerable to liquidity problems in the face of these heavy withdrawals.” 5 Sure enough, the Knickerbocker Trust was forced to close its doors on October 22 as they ran funds after handing over $8 million to frantic customers in three hours. The run on Knickerbocker spooked the public, and led to an outbreak of runs on other investment trusts.

“Other trusts, fearing the possibility of runs, began to call in loans and liquidate assets to build up their cash reserves. These efforts severely disrupted stock and bond markets, where securities dealers faced difficulties in financing the holding of their inventories, liquidity vanished, and asset prices fell.” 5

As markets plummeted and additional trusts collapsed, the already fragile credit market tightened further, which impacted the American economy. In 1907, the Wall Street Journal noted:

“It is obvious that every trust company is protecting itself to the full extent of its powers, and the small borrowers, however solvent, necessarily suffer at such a time.” 6

American corporations were also affected as countless companies relied upon investment trusts for financing and underwriting/distributing securities. This caused a decline in industrial production and capital expenditures, hurting industries like the railways particularly hard.

Conclusion

What we now call the Panic of 1907 was the most brutal recession in America until the Great Depression. The Dow Jones Industrial Average fell 37.7% in 1907, and was the final straw for American regulators. This panic directly led to the creation of the Federal Reserve as U.S. leaders looked for a way to reduce the fragility of American financial markets, and frequent ‘panics’ caused by gold shortages or shocks. Again, this all traces back to the San Francisco earthquake. Remarkable, isn’t it?

History is not a road-map, but a compass.

Reading all the financial history in the world will not enable you to predict everything that will unfold in financial markets. There is no historical road-map outlining the specific events that will occur today simply because of what’s happened in the past. However, history acts as an invaluable compass for steering investors in the right direction in challenging times. By recognizing the patterns that repeat themselves over the course of centuries, we can better position ourselves for whatever lies ahead.

The global economy and financial markets have only become more complex since 1907, which makes the knock-on effects of a catalyst like COVID-19 all the more potent and unexpected.

The knock-on effects of COVID-19 will likely be longer than most expect, because we have very little experience on which to base our expectations. For example, the political impact of this pandemic is yet to be seen, but will have a lasting effect. Investors should be cognizant of this reality despite what stock market performance might suggest.

The coronavirus and San Francisco earthquake are perfect examples of this due to their very similar ‘domino effects’ on the world, and impact on financial markets. Whether it’s the coronavirus pandemic leading to an airlines bailout and the quickest bear market on record, or whether it’s an earthquake in 1906 causing a European ally to raise interest rates to the point that it helped trigger a U.S. recession.

So what do we do as investors? There are three primary lessons. The first is that these unpredictable shocks remind us of the importance of diversification. If your investments were concentrated in British fire insurance stocks in 1906, or airline stocks like Boeing today, your portfolio was severely impacted. The second lesson is that once a catalyst occurs, there is no sense in wasting time on what you could’ve done differently to prepare. The best investors are those that will begin thinking about what the knock-on effects of the exogenous shock will be, and where they should or should not allocate their capital. Lastly, these types of shocks serve as stark reminders of why leverage reduces resiliency to unexpected events. Leverage is a double-edged sword, and can exacerbate already dire situations.

San Francisco’s earthquake and the coronavirus pandemic today demonstrate the importance of ‘calibrating’ your historical compass by studying how exogenous shocks and catalysts have unfolded before.

——

About the author

Jamie Catherwood is the author of the financial history blog Investor Amnesia and a Client Portfolio Associate at O’Shaughnessy Asset Management. You can follow him on Twitter at @jfc_3_

——

Agree or disagree with Jamie’s perspective? Have your own thoughts about the historical precedent for the current economic environment?

We would love to hear from you, and may feature your thoughts or questions in future pieces of content. Get in touch via the quick feedback form or email us at investments@fundrise.com.